The good news? Looks like the market has decided that the war is over, and everything will get back to “normal” pretty qiuckly. With stocks at all-time highs again, investors are pretty clearly expecting a peaceful resolution to this war, and fast, and President Trump said today that a real agreement with Iran is “mostly […]

Irregulars Quick Take

Paid members get a quick summary of the stocks teased and our thoughts here. Join as a Stock Gumshoe Irregular today (already a member? Log in)

The good news? Looks like the market has decided that the war is over, and everything will get back to “normal” pretty qiuckly. With stocks at all-time highs again, investors are pretty clearly expecting a peaceful resolution to this war, and fast, and President Trump said today that a real agreement with Iran is “mostly complete,” with the encouraging response that Iran has said they’ll open the Strait of Hormuz again because of the new ceasefire between Israel and Lebanon.

This matters not because markets care about war, (they usually don’t), but because they really care about food and energy prices and disruptions to key trade routes for critical commodities, and lots of things in the real global economy can fall apart the Strait of Hormuz stays functionally closed for a few months.

I’d say “peace is at hand, and energy markets will normalize by the end of the year” is probably “priced in” at this point… but, of course, neither the clear transit of the Strait of Hormuz this weekend nor the price of oil six months from now are really at all predictable today, this war has shifted pretty dramatically several times in its short life, and we’re also just starting to feel the typical inflationary impact of war. It is easy to be hopeful, and also easy to be wary of the next shoe to drop.

Meanwhile, President Trump is not backing down from his fight to prosecute Fed Chair Jerome Powell, which is purportedly about ‘cost overruns’ at the new Fed headquarters building in DC, but, of course, is widely perceived as the President’s way of pressuring Powell to either resign or cut interest rates immediately to boost the economy.

Powell isn’t backing down, either, noting that protecting the independence of the Fed means he can’t step down as long as this silly lawsuit still threatens the central bank — and so far, it seems like Senator Tillis is sticking to his guns and unlikely to allow a vote on the confirmation of President Trump’s nominee, Kevin Warsh, as long as Trump’s pressure on the Fed and this lawsuit are still active.

So that’s a three-way standoff, I guess — at a time when it’s pretty clear that inflation will be rising, at least temporarily, as the effects of the war percolate through the global economy… which is happening to a limited degree now, but, if energy and fertilizer prices continue to stay elevated, is inevitably going to get worse (after all, a little slice of almost everything we buy in a given week goes to cover the transport costs — which mostly means it’s driven by diesel fuel prices).

It’s pretty extraordinary, really — most of us are probably at least a little nervous, individually, about the risk that negotiations or the ceasefire could fail, or that this war could escalate into something far worse, despite good signs this week… but our consensus opinion, expressed through the stock market, is that everything will be just fine and there’s nothing to worry about. Markets are amazing.

At the same time, we’re back in the world of news-driven nuttiness when it comes to tech stocks, too — not only because of the fun story of Allbirds (BIRD), the formerly faddish maker of wool sneakers that went public with a $2+ billion valuation about five years ago, then gradually became irrelevant and went out of business, only to rebrand itself this week as an AI infrastructure company called, of course, NewBird AI, and start buying NVIDIA (NVDA) chips to lease out, becoming a “GPU-as-a-Service and AI-native cloud solutions provider.”

And we also had another week of quantum-mania, with all the more popular quantum computing stocks (IONQ, RGTI, QBTS, etc.) soaring 25-50% because NVIDIA released a new open-source AI model (called Ising) that they say might help quantum computers “improve calibration and error correction.”

I gotta tell you, even though it’s only anecdotal, but this is the kind of press release-driven stock movement that only ever seems to really catch our attention near market peaks, not during great buying opportunities. Like when Long Island Iced Tea decided to rename itself Long Blockchain in 2017, briefly soaring until the price of bitcoin hit its peak late that year and started to decline (bitcoin got back to those 2017 levels about three years later, but by then it was too late, Long Blockchain disappeared around 2021).

Story stocks are fun, it’s exciting to own a stock that goes up 50% for no real reason, and there’s always something to buy. Just remember that fun ones are the same stocks that can most easily decline 50% for no real reason. Maybe the best recent sign of sanity is that Oracle (ORCL) is back to a more “normal” valuation (~20X earnings), after flying too close to the sun with their OpenAI deal and massive AI spending plans last fall… or that the popular “pre-IPO” funds like Fundrise Innovation (VCX) and Destiny 100 (DXYZ) are back to trading at perhaps something closer to a reasonable premium to their net asset value, after soaring to 500%+ premiums at times because of investors’ desire to “get in before the IPO” on names like SpaceX and Anthropic. Who knows, perhaps the SpaceX IPO in a few months will really be the moment the market blows its top and begins to deflate. (I do not, of course, have any idea whether the market will rise or fall through the rest of the year.)

When in doubt, try to look at actual financials, including the real cash that moves into (and is consumed by) a business, and rational forecasts for what a company might be able to do over the next couple years, tempered by what you think the risk of loss is and how patient you’re willing to be. Trading stories and themes is exciting, but it will eventually come back to bite if you’re not great at it, or not nimble with your trading (I’m neither, usually), and periods of extreme performance tend to breed complacency, as we all forget that the long-term average return of the stock market is made up of great years and terrible years, with the terrible ones often coming pretty close to the great ones.

And yes, it has often felt nerve-wracking… but we’ve been through a fantastically great period recently — the Nasdaq 100, which is a silly index but widely followed, has returned 20.17%, 24.88% and 53.81% in the past three years. I’m pretty sure that the only three-year stretches for market returns that beat that were the three years before the Great Depression (the “roaring 20s”), the three years coming out of the Depression, before the breakout of WWII, and the late 1990s, going into the final blowout of dot-com mania.

That doesn’t mean we’re at the “top” right now, or that a “reckoning” is coming soon. Maybe the market will keep roaring for years, as new industries are created, perhaps from AI, and humans build products and businesses the likes of which we’ve never seen. There is certainly an optimist’s take to be considered here, too, nobody can really know, and every portfolio probably needs at least a little bit of optimism… but with inflation probably heating up and governments around the world so deep in the red that surprises (and more war) seem inevitable (which means more inflation, and more destruction of productive assets), and, more importantly, with valuations quite elevated in any historical context, even if they’re not as worrisome as they were five years ago at the 2021 peak… I have to think we should be cautious and have very low expectations for future growth.

Nobody wants to see a real washout, like a 50% market crash, but they do happen every now and then, they seem to play a pretty important role in washing speculation out of the system, and we haven’t seen that kind of downturn since the 2007-2009 financial crisis, and nobody is very good at predicting them. (The last two real market drops were in the 20-30% range, the initial COVID collapse of 2020 and then the inflation-driven collapse of 2022, but both were short-lived enough to prevent massive disruption, and they seem to have just taught investors to “buy the dip”).

So no, I don’t know if the market will fall sharply anytime soon, but it certainly could — and I’m trying to build my portfolio with the knowledge that the overall market returns for the next decade will probably be “meh,” with a reasonable possibility that we could see a “lost decade” when the broad stock market generates no return at all.

Calling to mind everyone’s favorite “complacency” meme:

I’m still quite fully invested, albeit with hedging and gold exposure and some meaningful diversification away from owning just the hottest growth stories in the market… but still, if I were within five years of retirement and needed to start living off of this portfolio soon, I’d probably be looking at ways to tap the brakes with my stock exposure. At least a little bit.

And now, with the potential end of the Iran war perhaps in sight, and maybe a gradual return to normalcy for the most disrupted markets (oil and gas, fertilizer, etc.), what will the stock market focus on next? Will we get back to worrying about private credit? The sustainability of AI capex spending for all those new data centers? Inflation or interest rates? Something entirely different?

We’ll see. Best to be ready for anything — keep those knees bent, keep your head on a swivel, the future will contain surprises.

Next up for our Real Money Portfolio is the busy heart of earnings season, in which we’ll hear from a bunch of our P&C Insurance companies next week, and from most of the big tech companies the week after that. Optimism and/or complacency remain high, but there’s a lot of room for the narrative to change pretty dramatically between now and early May. Heck, given the geopolitical situation, there’s a lot of room for the narrative to change between now and the market’s open on Monday morning.

So… what have we got to discuss today? We’ll start with a hodgepodge of thoughts on a bunch of our portfolio companies… and then I’ll spend some time digging into the stock I added to the watchlist yesterday, and briefly mentioning a second watchlist candidate.

*****

Amazon (AMZN) was in the news for a couple reasons recently… first because of the latest Letter to Shareholders posted by CEO Andy Jassey, and then because they bought Globalstar (GSAT), therefore instantly getting a “direct to cell phones” satellite business that they can build on through Amazon Leo, their Starlink competitor that should formally open for business in a couple months (after seven years of investment and satellite launches, with many more to come). That also ties Amazon in with Apple, since Globalstar has largely been funded by Apple in recent years, and is committed to supporting the satellite connectivity of iPhones.

What stands out in the Letter to Shareholders is just how committed Amazon is to building big businesses and trying to lead in new inflecting and disrupting parts of the market, (including by disrupting its own existing businesses), and their ongoing focus on the customer, with a relentless drive to take market share and grow markets by reducing customer costs. That’s always been how Amazon works, and investors have usually been patient with the time lag between Amazon’s investments and their return on investment, which is also the big worry many investors have about AI right now, so this is the part of the letter that got the most attention:

“We have customer commitments that make our capex investments predictable. We’re not investing approximately $200 billion in capex in 2026 on a hunch. The recent OpenAI commitment (over $100 billion) is an example of this, but there are several other customer agreements completed (and unannounced), or deep in process. Of the AWS capex we expect to spend in 2026, much of which will be monetized in 2027-2028, we already have customer commitments for a substantial portion of it.

“We are willing to make large capex investments and endure short-term FCF headwinds for the substantial medium to long-term FCF surplus. AI is a once-in-a-lifetime opportunity where the current growth is unprecedented and the future growth even bigger. AWS has a significant leadership position with the broadest functionality, strongest security and operational performance, largest share of customers and revenue, strong desire from customers to run their AI in AWS, and an opportunity to build what could be a new pillar for Amazon in chips. We’re not going to be conservative in how we play this—we’re investing to be the meaningful leader, and our future business, operating income, and FCF will be much larger because of it.”

The letter is definitely worth a read — lots of companies post shareholder letters now, but Amazon has always been one of the best at really outlining and explaining their strategy in those letters, reinforcing investor commitment to that long-term vision. Still a phenomenal company, and if you’re interested in buying it’s been below my “max buy” price ($258) for a long time… though it’s been quietly creeping up to that level recently, so it might not be ‘buyable’ forever.

And Amazon Autos keeps growing, too — that business was announced in late 2023 but didn’t really get going until they started selling new Hyundai cars through Amazon in late 2024, directed to local dealerships, and now that has unsurprisingly grown to include Hyundai’s cousin Kia, but has also made a leap to include Chevrolet and Jeep from Stellantis (STLA), which boosts the variety considerably. Since few people seem to like the in-person car purchasing process, I’d expect this to continue. Seems like Amazon might be able to build a whole new Carvana (CVNA)-like business without breaking a sweat, though, of course, there’s always some advantage to being the company that cares most about your market, and auto sales will likely never be a market Amazon cares more about than Carvana.

Incidentally, when it comes to the “space race” part of tech-world and the battle for LEO broadband services, we’re also reminded that Alphabet (GOOGL, GOOG) owns ~$100 billion worth of SpaceX (that’s assuming it’s really a $2 trillion company, as many folks expect it will be when their IPO is priced later this year — Alphabet’s SpaceX ownership is just over 5%, second only to Elon Musk’s personal stake).

And speaking of Alphabet, it’s being widely reported that Meta Platforms (META) will surpass Alphabet (GOOGL) in ad revenue this year, as Instagram and Facebook continue to benefit from AI-driven advertising placements and creatives. Which is a little surprising, but I guess it underscores the ongoing rise of social media and how ad-choked it has truly become, with AI helping that process along. I imagine that will be the talk of the town soon, since Meta, Alphabet and Amazon are all expected to report on the same day this quarter, April 29.

*****

The acquisition of Peets is now just about complete for Keurig Dr Pepper (KDP), as expected.

And we’re starting to hear more about the state of the beverage industry at the moment, starting with the quarterly report from PepsiCo (PEP), which highlights some ongoing recovery in convenience stores… so that’s helpful for both KDP’s ongoing turnaround and for our hopes of volume and revenue growth for Celsius (CELH), which manages most of the energy brands that are distributed by Pepsi (Celsius, Alani Nu and Rockstar). Here’s what they said on the PEP call that is at least relatively encouraging after some challenging years:

“Now, what’s exciting about PBNA (Pepsi Beverages North America) at this point is that the business grew 9%. Now, it’s a combination of organic growth, a revenue growth of 2%, plus 7 points of additional platforms that are now in our distribution system. Some of that is business that we acquired, like poppi. Some of that is an increased portfolio of energy brands that are generating growth to our business. We feel good about the 9%.

“We feel good about the acceleration, the 2% inorganic, and we feel good about the fact that we have flat volume ex case pack water, and that progress, that acceleration will continue in the coming quarters. Our expectation is to have positive volume growth ex case pack water in the coming quarters….

“We see ourselves participating in the energy portfolio through our Celsius investment and our distribution of Celsius. That’s gaining share.”

Doesn’t mean Celsius will have a great quarter, there’s been lots of lag and uncertainty with how the distribution works (as we recall, Celsius had a great start to the year a couple years ago because Pepsi was filling out its distribution channels… but it turned out that they over-ordered and it took more than a year to “normalize” inventory, testing the patience of investors).

Keurig Dr Pepper should report on Thursday morning next week, with analysts pretty sure both that the quarter will be “fine” and that most of the news, and the potential catalysts, are going to take a few quarters to emerge (mostly due to the expected separation of the coffee and beverage businesses — which, along with the 3.5% dividend while we wait and the growing brand value of Dr Pepper, is why we’re in the stock)… and Celsius reports a couple weeks after that, so we’ll soon see how our holdings are, well, holding up… but Pepsi at least indicates that the sector is doing OK at the moment.

****

Progressive’s (PGR) earnings reports is always a little strangely timed, since they report most of the key information every month, not just once per quarter — so we now know how the first quarter went, because we got their March earnings, even though they haven’t actually filed their quarterly earnings yet.

And it’s in the “pretty good” category at this point. Continued net premium growth, solid earnings, no real change to my thinking. They continue to have a strong combined ratio, still in the ~86% range for the quarter, they continue to see policy growth, with most of that led by direct auto policies sold (direct as in not through an agent, with agent sales growing more slowly), and their total revenue continues to grow. The risk is that analysts continue to believe that we are right at the peak in earnings, and earnings per share will decline to ~$16 (from $18 last year), and will remain relatively flat for a few years.

Things could play out that way, of course, auto insurance is competitive and Progressive’s long-held technological lead has probably eroded. They likely won’t “win” every battle against State Farm and GEICO and others, and, importantly, Progressive has so far had trouble growing their non-auto coverage (they’d like to get more into homeowners’ coverage, too, through “bundling”). Still, they’re also extremely well run, have consistently led the market, and I suspect they’ll do better over the next few years than analysts expect, if only because a stable market should mean that they have very high policy retention… and at 12X forward earnings (10X trailing), we’re not leaping over a high hurdle.

This is still one we need to think about differently — like Kinsale (KNSL), Progressive is a high-profit and low-cost market leader with historically above-market growth (though Kinsale growth has been far more extreme than Progressive, and is also slowing down more rapidly)… which means we can be a little more flexible and judge it as an earnings and earnings growth story if we believe they can sustain their market leadership (Progressive in direct auto, Kinsale in smaller E&S policies), rather than judging them like I do most other insurance companies, based on book value and likely compounding from both profitable underwriting and investment returns over much longer periods of time.

But the risk is that if we’re wrong about Progressive’s ability to sustain that market share and high earnings, based largely on low expenses, and earnings really drop meaningfully because of competitive pressures (or anything else), then they could have a ways to fall. I usually think of insurance companies relative to their book value plus insurance float (the money they have collected from policyholders, and earn returns on, but don’t own and theoretically will have to pay out in claims at some point), and on that measure Progressive has a “book + float” of a little over $100 billion, and trades at a premium to that (market cap around $120 billion — so if this were a more diversified P&C insurer like Chubb (CB) or W.R. Berkley (WRB), Progressive wouldn’t be appealing until it dropped to about $75 billion, I like a 25% discount to “book + float” for those kinds of companies… if we were to wait for that, I wouldn’t buy Progressive unless it fell to about $130). And Progressive is also trading at about 4X book value, which is a valuation most insurance companies can’t sustain (again, other than Kinsale, thanks to its high growth).

So I still expect it to work out well, I think they’re more likely to sustain their earnings than to fall by 10% or so this year, as analysts are currently predicting, and I don’t see any reason why the industry leader should lose ground — but if they do, it could be risky. No change to my “buy under” levels (max buy is still $225), and this Progressive position is still small and roughly breaking even in the Real Money Portfolio, but I’m more likely to buy a little more than to sell if things stay as they are.

*****

This week started with rumors about NVIDIA (NVDA) acquiring a hardware company, most likely Dell (DELL) or HP (HPQ), though NVIDIA shot down those rumors immediately. And there was also some speculation that Intel (INTC) and AMD (AMD) might combine, since Intel has been unable to beat AMD and AMD, at least in the opinion of some investors, needs to do something other than just keep chasing NVIDIA.

I don’t know that any of this is true, but those are the narratives being chattered about among the MBAs who can’t stand the idea that anyone will go a month without talking about acquisitions and synergies. This is what happens when bull markets go haywire — investment bankers and companies begin to look to extreme acquisitions to catch the attention of investors and/or help build an empire. Big deals in hot sectors, done at rich valuations, don’t often lead to happiness.

*****

Hershey (HSY) has been finally drifting down more toward ‘reasonable’ lately — and, interesting enough, the big commodity chocolate provider, Callebaut, has been talking about the challenges of the chocolate market… not because cacao prices are rising, as was the case a couple years ago, but because they’re falling, which is a challenge for them because they’re at a different point in the supply chain than Hershey, and may have to sell processed materials at a loss, at a time when end user demand is fairly soft. This is a little excerpt of the FT story on Callebaut:

“Swiss chocolate maker Barry Callebaut has cut its profit forecast and warned of the effect of falling cocoa prices, industry overcapacity and supply disruptions, sending its shares down more than 15 per cent.

“The Zurich-based group said it now expected earnings before interest and tax to fall by a “mid-teens” percentage in its current financial year, reversing earlier guidance for growth and underscoring the scale of the challenge facing new chief executive Hein Schumacher….

“Analysts said falling cocoa prices had yet to feed through to retail chocolate prices, which remain high and continue to weigh on demand. “It takes time for this cocoa collapse to feed into high street chocolate prices,” said Cox, adding that high street prices were up about 10 per cent compared with a year ago.

“Despite the weaker earnings outlook, Barry Callebaut said it expected volumes to recover in the second half of the year and now forecasts a smaller full-year decline of between 1 and 3 per cent, with a return to growth thereafter. Cocoa prices, which have more than halved in recent months, should be ‘supportive for future market recovery’, it added.

“Cox pointed to longer-term risks to demand, including the rise of GLP-1 weight-loss drugs. ‘In a GLP-1 world, how much will chocolate volumes still grow?’ he said, noting that Barry Callebaut’s business has historically relied on high volumes.”

Those GLP-1 drugs and the overall consumer weariness from inflation are the two primary issues that seem to worry investors in packaged treat companies like Hershey, and the risks are real. I just went on Zepbound about a month ago, trying to lose some weight to give my arthritis a break, and hoping that doing so might let me delay hip replacement, and I can certainly say that I’m eating less chocolate and drinking less whiskey. But I think we’re a long way from knowing whether this will have a sustained global impact on food and beverage companies, and I would guess that investors are probably over-worrying about risks.

But the lower prices for raw chocolate? Those are really just beginning to boost Hershey’s bottom line, even as they hurt Callebaut’s, so the declining HSY share price over the past few months carries some appeal (down ~17% from the late February peak… and, more importantly, now dipping well below my $209 “max buy” level). Even if we’re already past one of the key periods for Hershey sales, with the easter holiday coming pretty early this year. And the 3% dividend will at least help a little bit, keeping us warm on any chilly days to come.

Hershey will report in a couple weeks, too, should be on April 30.

*****

Toast (TOST) announced the availability of a package of drive-thru management software and equipment for quick service restaurants… which seems like yet another shot across the bow for PAR Technology (PAR), since enterprise quick service restaurant chains are its core business and drive-thrus dominate that sector.

These days, with their proven ability to operate at scale and improve margins while PAR has been unable to reach scale and keeps frustrating shareholders with more acquisitions, Toast remains the much easier buy, and is more likely to see AI-enabled growth than to become an AI victim (though I do continue to hold PAR, which similarly should not be terribly threatened by AI, and which has been clobbered for a suite of reasons we’ve discussed many times).

Of course, if the economy sinks into a quagmire because of inflation and high gas prices, and people stop eating out, everything suffers — that kind of environment has historically favored the fast food chains over higher-end chain and local restaurants, but it’s also true that bigger chains like McDonald’s are selling meals at prices which are now much more comparable to many “sit down” restaurants than in the past, fast food is not “cheap” for most people… so we’ll see if that pattern repeats.

*****

Bill Ackman’s road show for his new Pershing Square USA (PSUS) fund continues to chug along, and he’s been pretty successful at attracting attention, even in this very distracting market environment… and yet, still, Pershing Square Holdings (PSH.L, PSHZF) continues to trade at a 30% discount to net asset value (it has narrowed to near 20% a few times in the past six months, but never more than that). That means it’s going to be a tough swallow to consider buying into PSUS at net asset value, even with the “10% bonus” of the shares of his core company, the asset manager Pershing Square, thrown in to entice investors.

It will be really interesting to see if PSUS prices OK and holds its IPO value when it starts trading — which is probably also likely to happen the week after next, likely on April 28 or 29. Another test of Bill Ackman’s ability to sell himself — his halo has been fading at Howard Hughes (HHH) and Pershing Square Holdings, at least for now, but HHH is still not even in the first inning of the game they’re hoping to play, the overall investment returns at Pershing Square Holdings remain pretty good (even if I’ve been shrinking my stake in that fund, as it more closely mimics my own investments and therefore offers less and less diversification)… and Wall Street’s Thin White Duke remains undeterred.

Adding to the Watchlist

And there are two new watchlist entries this week — one I wrote briefly about yesterday, Uranium Royalty Corp (UROY, URC.TO), which is making a transformative acquisition… and one I haven’t dug into as deeply yet in Forgent Power Solutions (FPS), which is a mashup of transformer companies that was funded by private equity and went public earlier this year.

Forgent I’ll wait to get into more detail with in the future as we head into the IPO lockup — that lockup expiration should be August 4, 2026, six months after their February IPO, but this is my quick summary:

I suspect that the real question with Forgent is whether the current spike in demand for power transformers, both to upgrade the grid and the build new data centers, is sustainable… and whether Forgent itself has some potential to really grow earnings, or is just a good “theme” story sold to us by private equity, right near the peak of that business. The company was created by Neos Partners, a private equity firm, engineering the merger of MGM Transformer Co., PwrQ, States Manufacturing, and VanTran Industries, with most of the deals happening just a year or two ago, so it’s been a really fast “roll up.”

I’m not really sure what the answer is, but the track record is short and the valuation is pretty high, which is why I haven’t gotten more interested yet, despite the pretty compelling theme of “we just can’t make enough electrical equipment to meet demand.” And there’s a dual-class share structure, so Neos Partners is still in control, with more than 50% of the vote and ~$5-6 billion worth of shares still owned, even after they sold a good chunk into the IPO in February, so I’m wondering whether some larger insider sales at lockup time might bring the valuation down (after which we’ll also have seen some more quarterly updates, to give us a better idea of where the business is headed). I’ll keep an eye on it and let you know.

But I have spent some more time on the Uranium Royalty story over the past 24 hours or so.

I shared some initial thoughts about the new and improved Uranium Royalty (UROY, URC.TO) yesterday, when the news broke of their big deal with Sweetwater Royalties, and I’m putting that stock on my watchlist — it’s still pretty expensive, but I like the potential that Sweetwater might eventually bring to this portfolio, particularly if uranium ends up being a relatively stable commodity for a while, with increased production and increased consumption as more new reactors begin to inch toward the start of construction in the US and overseas.

Here’s what I’ve cobbled together for you as my initial thinking about this combination, after going through the announcements and filings a bit more and thinking about the things they said in the presentation announcing and explaining the deal.

This is the sum-up from UROY’s CEO Scott Melbye:

“URC enjoys its royalty and streaming leadership in the uranium space, a strong balance sheet and liquidity profile, a highly experienced management team, and a portfolio of high-quality uranium royalties with unhedged price upside. What it lacks is more robust near-term cash flows while the uranium market rebounds from its historic bear market and the portfolio begins to crystallize in value.

“Sweetwater couldn’t fill this gap any better, with immediate cash flow from world-class assets in a top jurisdiction, significant growth without additional incremental capital, and an enormous untapped growth through the second largest public company land position in the United States. In other words, the Sweetwater combination gives the new URC the financial base and wherewithal to fully realize its uranium growth ambitions at a time of epic expansion in nuclear energy.

“Put simply, this combination adds significant cash flow and strategic land holdings to accelerate Uranium Royalty growth. It increases URC annual EBITDA to approximately $74 million and immediately positions URC as a cash flowing company from well-established royalties from mines in the world’s leading trona jurisdiction that will see production for 100+ years. These are leading assets in the first quartile of total production cost.”

That cash flow is certainly helpful for Uranium Royalty, and that’s a pretty fair estimate of reasonable cash flow — they say that, “the last two years of pro forma attributable EBITDA would have averaged $74 million. 2025 was a bit lower as a result of mining on checkerboard quadrants of federal land, and this year’s return should gravitate back towards the average.”

So that should mean they have some exposure to any potentially higher commodity prices, but they’re not counting on higher prices to generate that $74 million.

So that sounds pretty rational as the starting point for EBITDA calculations, even though it comes at pretty meaningful cost and is attached to a pretty big chunk of debt (which is being paid down, mortgage-style, through steady amortization, so it’s not just the interest cost, and that means the cash flow impact is pretty meaningful)… and if all the potential expansion projects and new operations that they know about come online, they do see the potential to roughly triple that cash flow.

In their words, “Between brownfield expansions and optimization of existing mines and advanced greenfield projects at Pacific Soda and West Soda, there’s potential for as much as 14.7 million tons of production per annum in the coming years. This would result in almost three times increase in EBITDA.”

So production could grow “in the coming years,” but the interesting longer-term optionality (maybe much longer, to be reasonably cautious), might be in the large land portfolio. As they put it, “this transaction represents an unprecedented land opportunity. 850,000 acres in surface fee land and 4.5 million acres of mineral rights in fee. Not just anywhere, but in the resource-rich and development-friendly jurisdictions of Wyoming and Utah.”

So unlike most royalty companies, Sweetwater Royalties is a huge land owner, not just an owner of mineral rights, which means they can also pitch themselves with a comparison to giants like Texas Pacific Land (TPL), which found surprising value in its land decades after that land first went into what was then an investment trust (now a corporation). And maybe that will be the way things go for the new Uranium Royalty, maybe there’s a lot of value to be harvested from that huge land holding… but what’s of value so far is the known and producing (or in development) mineral assets.

And that’s the bad news, sort of. Sweetwater Royalties may have the potential for meaningful uranium royalties someday, given that there are uranium in situ recovery (ISR) projects in similar areas in Wyoming… but right now, the cash flow for Sweetwater comes from the royalties they earn from soda ash, produced from their huge trona resource in Wyoming. They own some of the biggest soda ash resources in the world, and by far the largest natural source — about 90% of the soda ash used in the US ( and about 25% of world consumption) comes from the Green River Basin in Wyoming, about half of it from Sweetwater’s lands and paying a royalty to Sweetwater, so it is a genuinely long-lived and critical resource.

Soda ash is critical, and there isn’t a great replacement — it’s needed for glass production, detergents, water treatment and other chemical end markets… but it’s not really scarce, and it hasn’t been rising in price — China makes a ton of soda ash, too, much of it synthetically, and prices have been under a little pressure this year… which is perhaps why Sweetwater was willing to sell.

The Wyoming trona deposits are a valuable long-lived resource… but they’re probably best seen as a steady resource, the royalties might grow if planned and under-construction expansion projects move forward to expand capacity over time, but this is not likely to be a commodity that spikes in value or generates cash windfalls anytime soon.

So yes, Uranium Royalty gets some meaningful cash flow out of this, and that could be a valuable reset for the company and help them scale up… but they’re not getting a lot of instant uranium-derived cash flow, it’s all coming from soda ash. And Uranium Royalty’s own uranium-derived cash flow right now is relatively paltry, to the extent that it will be probably be less than 20% of the revenue of the combined company… with growth potential, but not a lot of clarity on when new mines might get built and begin to generate that cash flow growth. As a real uranium royalty play, this new company will still really be a startup — just one with a big debt position that’s serviced by meaningful cash flow from Sweetwater, and with whatever other optionality that Sweetwater land and mineral rights portfolio might provide.

Here’s how they describe the resource — this excerpt from their conference call is a little long, but it’s worth getting the perspective, especially for someone like me who doesn’t know anything about soda ash:

“The soda ash market has grown from approximately 61 million tons in 2015 to around 79 million tons today, which equates to about a 3% annual growth rate over the past 10 years, with the overall size of the market growing by 30% or 18 million tons per annum in just the last 10 years. Looking forward, demand driven by the energy transition is forecasted to continue growing in the near term from 79 million tons to 92 million tons per annum in 2030.

“Put simply, that equates to about 13 million tons per annum of additional soda ash being needed between now and 2030, with about 8 million of those tons per annum forecasted to come from increased solar glass and battery demand, as soda ash is the preferred carbonate for making lithium carbonate. As we turn to the next slide, it’s worth keeping the scale of growth and forecasted growth front of mind.

“We’ve seen 18 million tons of demand growth over the past decade, with a further 13 million tons per annum expected to be needed by 2030. Against that backdrop, let me show you where a meaningful portion of that future growth is expected to come from. Sweetwater’s trona mineral state is in an area designated as the Known Sodium Leasing Area, for short, the KSLA. It’s in the Green River Basin of southwestern Wyoming.

“The area is also known as the Snowman. A look at the map will tell you why. The KSLA holds the world’s largest known trona deposit, estimated to be 90% or more of the world’s known trona reserves and resources. Today, there are five producing mines operated by four high-quality operators, collectively mining approximately 20 million tons of trona annually to produce approximately 12 million tons of soda ash annually.

“Sweetwater owns approximately 50% of the minerals in the KSLA in a checkerboard fashion with federal and state lands. While production and sales volumes from our lands can vary from year- to- year, as a percent of total production and sales from the basin, we have generally received a royalty on approximately half of the soda ash production and sales from the basin. Stepping back, the size of Sweetwater’s minerals and strategic significance here is hard to overstate.

“Sweetwater owns approximately half of the minerals in the KSLA, i.e., approximately 45% of the world’s known trona, and the mines in the basin are firmly in the first cost quartile globally. That combination of size, scale, cost position, and resource longevity underpins the long-term durability of our royalty income. What’s particularly compelling is that this is not a static asset. Across the basin, we’re seeing ongoing brownfield expansions from existing operators alongside two advanced greenfield development projects.

“That provides visible long-term production growth without any capital requirements from us. Importantly, beyond the current producing and under development footprint, Sweetwater also owns significant unleased mineral acreage within the KSLA, which provides additional opportunities for future development and royalty generation. In summary, the KSLA represents exactly what to look for in a royalty asset, long life, low cost production, operated by high quality counterparties with embedded organic growth and no capital exposure.”

That’s inherently appealing… but it doesn’t necessarily mean investors will get excited about it. Altius Minerals (ALS.TO, ATUSF) has similar heft in the potash market, with royalties on some of the biggest potash mines in the world, with 100+ years of production ahead… but when potash prices are unusually low, as they often have been in recent years, investors don’t get all that excited about that asset. Owning a royalty on a 100+ year asset should be a fortune builder for a patient investor, assuming you didn’t overpay for it, but it’s not necessarily a “get you rich in the next five years” kind of fortune, and the stock market can change its mind about those kinds of assets with some regularity, often ignoring them for years at a time if prices or production aren’t growing.

And the uranium potential of the Sweetwater lands? Seems like it’s probably there, primarily just because “Wyoming has a lot of uranium,” but it is not going to be a driver of results anytime soon — this is from the UROY’s CEO (my emphasis):

“I can say without a doubt that this Sweetwater land position across the entire southern portion of the state from Cheyenne to Salt Lake City represents significant uranium optionality. Wyoming has multiple uranium companies in operation and has accounted for over 70% of historic US-mined uranium, cumulatively over 250 million pounds to date.”

The only specific they really share is that ongoing surveys are “yielding prospective uranium regions across Sweetwater land.”

If you’re keeping track, “optionality” is maybe half a step from “prospective region”… but those are both a mile down the road from “discovered uranium” and a couple exits on the highway down from “defined resources.” And a discovered resource base itself still means you’re across the county line from “viable reserves” that might, if the financing can be raised, become a uranium mine. There is a road to Sweetwater’s land becoming a uranium royalty region, but it’s probably a very, very long road.

The existing controlling shareholders of Sweetwater, Orion and the Ontario Teachers Fund, will get some cash payout (totaling about $300 million), but will also own ~60% of the new Uranium Royalty Corp. There won’t really be much in the way of “efficiencies” generated by the merger, since the two companies are both keeping their management teams and will operate separately. The deal should pretty easily be approved in the shareholder vote, I would expect, which means it will probably close sometime in June.

And when it comes to the actual cash flow from UROY’s uranium projects, the things they owned before this deal closed? Here’s what they said on that front:

“Looking to the future, analysts’ forecasts see cash flows reaching roughly $15 million by 2030, ramping up to $38 million in subsequent years.

“We should also not lose sight of the fact that URC physical uranium purchases made off the bottom have generated $89 million in cumulative gross revenue, with $20.2 million in gross profit.”

So yes, you can see the appeal of adding Sweetwater’s cash flow — Sweetwater Royalties generated an average of $74 million in EBITDA over the past couple years, and during that time Uranium Royalty generated an average of about $1 million in EBITDA. They haven’t really gotten going on that front yet. Despite having royalties and NPI deals for some producing uranium mines, including both of Cameco’s big mines in Saskatchewan (a 10-20% NPI on Cigar Lake, and a 1% GORR on McArthur River).

And when it comes to investor thinking, 2030 is still a long way away — so what would we pay for $15 million of royalty cash flows in 2030? I wasn’t willing to pay even $200 million for that on the few times I looked at UROY over the past several years (that’s roughly where the market cap has bottomed out for them over the past five years), and paying $500+ million for it now seems awfully extreme… but maybe now that they’ve added the Sweetwater soda ash cash flow to that, perhaps it could become appealing?

Maybe… but then we get to the debt which comes along with the deal — here’s how they describe that:

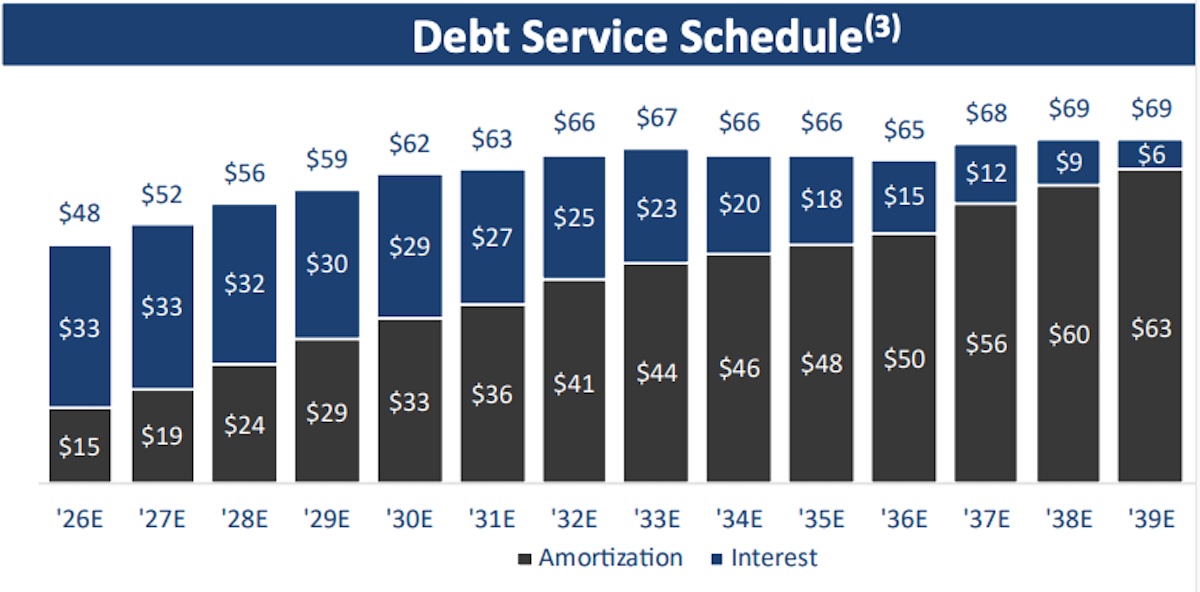

“The transaction does require that URC absorb Sweetwater’s debt facility. Fortunately, this facility has an attractive coupon rate of 5.3% under a long-dated mortgage style amortization. It has a BBB rating and is held by a group of life insurance companies.”

OK, so yes, that sounds like a rational debt to hold… but investors are really used to thinking only about the interest costs of debt, not paying it off, and the amortization schedule of this debt means it also eats a lot of the cash flow. This is the debt service schedule from the company — remember, at this point, they are producing about $74 million in EBITDA, so 2/3 of that is already spoken for (Interest is the I, and Amortization the A in EBITDA, so you can see why they keep emphasizing the Earnings Before (EB) those items):

What they really want us to look at, though, is the big-picture optimism about nuclear power:

“Suddenly, the World Nuclear Association’s aspirational goal of tripling of nuclear power by 2050 looks rather achievable. In fact, forecasts are already trending towards those levels. However, at the same time, the post-Fukushima bear market failed to produce meaningful investments in uranium exploration and new mine development, which has created a massive 1.7 billion-pound supply deficit between now and 2045. I believe Goldman Sachs pegs this closer to 1.9 billion. As a capital provider for new mine development, this is the looming opportunity for URC to capture a portion of the billions of dollars in capital required to close the deficit gap through royalties and streams. The Sweetwater combination gives URC the financial wherewithal and near-term cash flow to successfully realize on this opportunity. URC’s mandate has been and will continue to be laser-focused on growth in the dynamic global uranium space.”

It’s good to have a viable uranium royalty company available, but it’s starting to look to me like UROY isn’t ready yet. Almost all of their cash flow over the past year or two has come from buying and selling uranium, not from their uranium mine royalties, and the growth from their uranium royalties is very likely to remain pretty minimal for at least several years (well, minimal for a $1.5 billion company with $600+ million in debt, at least).

The only projection they make for the uranium royalties is that they say analysts expect them to reach $15 million by 2030. At that point, unless things change in a material way, the hope is that the soda ash royalties will be generating close to $200 million in EBITDA… so without a huge surge in pricing for either soda ash or uranium, or some radically sped up uranium mine development from their royalty partners, that means this will be a soda ash royalty company for the foreseeable future.

Maybe that’s worthwhile, and the soda ash royalties are a meaningful long-lived asset, but I’d have to be a lot more certain of that “production could triple” to reach ~$200 million growth forecast to be willing to take on this debt and the high current valuation.

And more importantly, I suspect that their uranium focus means they’ll be working hard to build the uranium royalty portfolio, which will mean diluting that growing soda ash cash flow and using that cash flow to invest in expanding the uranium royalty portfolio. The risk there is that the cash flow probably won’t be enough to really buy any assets that can boost their uranium cash flow over the next five years, so my fear is that they’ll be ambitious about trying to strike new uranium royalty deals, which will take capital, and they’ll raise that capital by selling more shares, hoping they can do so more easily as a $1.5 billion company than they could as a $500 million company. We’ve seen what happens with royalty companies who get too ambitious about buying future growth, especially if the market happens to go through a “down” cycle for pricing of their commodity (either soda ash or uranium, in this case) — that’s the Sandstorm Gold story of much of the past decade, dilutive empire building that angers investors and depresses valuation, and I am inclined to wait to see what they’re “uranium growth” strategy is like before I sign up for that kind of ride again.

This is the part where I can see the argument for a re-rating higher for UROY shares, but I’m not sure I believe it:

“This combination will bring a 5x increase to the standalone enterprise value of URC. The significant increase in NAV, coupled with the lowest multiple in the peer group, should create huge potential for a re-rating in share price. Finally, this combination is expected to unlock meaningful upside through value recognition of the strategic land position.

“Just look at the enterprise values of Texas Pacific and LandBridge at $36 billion and $6.5 billion respectively. Compare to the new URC’s pro forma EV of $2.1 billion and its uncomparable 5.35 million-acre land position. Other measures like EV dollars per acre, EV to EBITDA, and recent EBITDA to total acres all point to a significant re-rating. In closing, I hope you’ll agree that this is a transformational combination, creating an investment opportunity that doesn’t come along in capital markets very often.”

What’s the problem with that argument? Well, first of all the debt part of that 5X increase in enterprise value, which reduces their optionality and means they will proably not have a huge amount of surplus cash available to serve as a “financier” to uranium companies in the next few years… not unless they either ramp up the debt further, or dilute shareholders by selling stock.

And second, of course, is that land in Wyoming and land in and around the Permian Basin in West Texas are not the same thing. You can probably buy land in the Green River Basin for $1,000 an acre, but buying even just mineral rights (not surface rights, which also means no water rights) in the Permian Basin might cost you $20-50,000/acre. Those are wild generalizations, and may be off by a lot, land values vary dramatically even within each of those areas, but you get the idea. Land is land, but location matters.

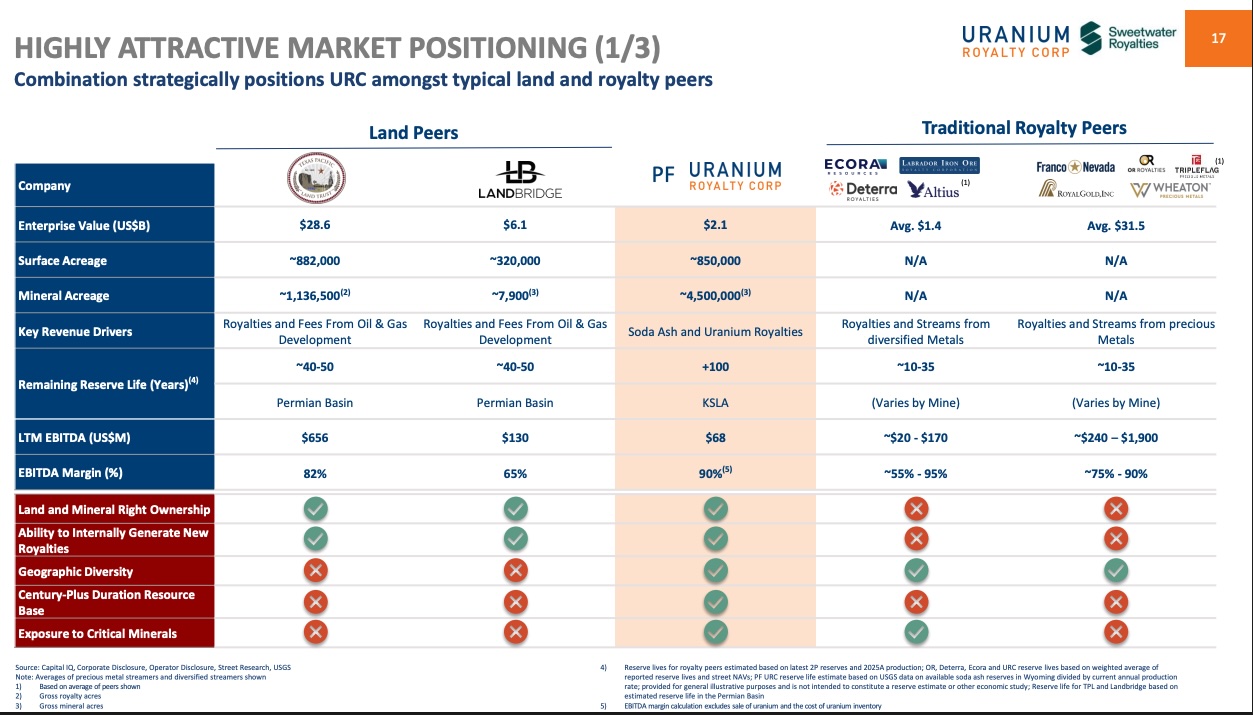

So the goal is to compare them to the “land peers” (TPL and Landbridge (LB), they say) and the “royalty peers” (both the gold ones that we follow often, and the base metal/diversified players like Altius and Ecora Resources, which we’ve owned in the past) — and I’m afraid they may flatter themselves too much with this slide:

All of which brings us to my opinion: Which is that I still find this interesting, and I’d love it if there were a real uranium royalty company that I was sure could generate meaningful cash flow from uranium over the next five years… but UROY isn’t that, at least yet, and that debt is eating up too much of Sweetwater’s expected cash flow to make boosting the uranium cash flow quickly seem like a feasible goal.

I’m afraid that the growth of the uranium portion of the portfolio is likely to be very slow, and, going by the tenor of the presentation, that means they’re going to be tempted to boost that with acquisitions. Which, given their debt level, probably means using their shares to buy royalties. Which increases the risk, particularly if it happens in a year when soda ash or uranium prices, or production (on their royalty lands), are flat or falling.

The big thing that really stands out as different from most of the established royalty companies, unfortunately, is that a huge portion of New Uranium Royalty Corp’s EBITDA is going to I (interest) and A (amortization), and therefore can’t really fall down to become cash flow that they can use… and that’s just not the case with almost any of the other comparison companies on that slice, both because they don’t carry debt which is anywhere near this onerous, and because the big driver of high EBITDA for most of the established royalty companies is not I or A but D (depreciation — or really, in their case, depletion of mineral reserves). Unlike interest and unlike the amortization for UROY’s loans, depreciation and/or depletion is a non-cash expense. We can argue about whether or not it’s “real,” one reason why people hate EBITDA is that they know companies do have to reinvest to

That eats into the “optionality” too much, in my opinion, so I’m going to keep watching UROY because I want to like it, and I like the idea of it… but the valuation just doesn’t make sense to me today. I see that there’s a rational argument to be made for paying 30X cash flow for a 100+ year royalty on a steady resource, particularly because there’s growth potential, but given the rising interest and depreciation charges, and the high level of debt relative to their incoming revenue, 30X EBITDA is a LOT, especially if we’re a little bit worried that they’re going to be tempted to grow the uranium part of the business more quickly by diluting shareholders.

*****

And I expect you’re pretty sick of hearing me say that gold royalty companies are the best way to invest in precious metals… so I’ll borrow the words of someone else who’s saying the same thing this week, this is some PR from UBS, which just started coverage of some of the big players:

“Gold streaming and royalty companies offer better growth and a stronger hedge against cost inflation than gold miners, with more stable margins and lower execution risk, UBS said in a note Wednesday.

“The analysts said that during the gold price upcycle last year, miners offered higher operational leverage to metal price upside, while inflationary pressures remained moderate and companies appeared less likely to miss guidance. At the same time, streaming companies like Franco-Nevada (FNV), Wheaton Precious Metals (WPM), and Royal Gold (RGLD) became cheaper relative to their historical valuations, they said.

“Looking ahead, gold prices are still expected to remain strong, but not rise as sharply as they did in 2025, the analysts said. Meanwhile, miners may face increasing cost pressures, especially from energy and potential disruptions, which could hurt margins, they added.

‘We believe [Franco-Nevada, Wheaton Precious Metals, and Royal Gold] all offer superior near-term and medium-term growth prospects versus most large cap miners,’ the analysts said.

“UBS reiterated its buy ratings on Franco-Nevada with a $310 price target and on Wheaton Precious Metals with a $160 price target, and initiated Royal Gold with a buy rating and a $325 price target.”

My prediction? If silver soars again, Wheaton will lead the way… if Cobre Panama reopens at full scale, Franco-Nevada will lead the way… if neither of those things happen, Royal Gold is a much easier buy at current valuations. I can’t predict the future, so I have exposure to all three… but much more exposure to Royal Gold.

And that’s all for this week, dear friends — I’ve gotten some questions about the Brookfields recently, so I’ll look into what thoughts I can share about those companies in the weeks ahead, and we’ll be inundated with new earnings reports before you know it… hopefully the world will be at peace, crises will fade, and we’ll all be able to focus on those earnings reports as the core driver of the stock market in the weeks to come.

Disclosure: I own all of the companies mentioned in the Quick Take as being below “buy” prices. Of the companies mentioned in the text of the article, I own shares of and/or call options on Franco-Nevada, Wheaton Precious Metals, Royal Gold, PAR Technology, Toast, Pershing Square Holdings, Howard Hughes Holdings, Hershey, Amazon, Alphabet, NVIDIA, Progressive, Chugg, W.R. Berkley, Keurig Dr Pepper, Texas Pacific Land, and Celsius Holdings. I will not trade in any covered stock for at least three days after publication, per Stock Gumshoe’s trading rules.